The Federal Housing Finance Agency (FHFA), now under the leadership of Bill Pulte, is moving to reverse a highly contentious set of changes to mortgage pricing known as loan-level price adjustments (LLPAs). The announcement is reigniting debate over whether the 2023 updates—intended to increase equity in housing finance—went too far in penalizing qualified buyers with strong credit scores.

At the heart of this Fannie Mae LLPA controversy is a proposed rollback that could meaningfully alter how mortgage fees are calculated for millions of borrowers.

What Are LLPAs, and Why Did They Spark Backlash?

Loan-level price adjustments are upfront fees charged by Fannie Mae and Freddie Mac to account for loan risk factors such as credit score, loan-to-value (LTV) ratio, and occupancy type. Introduced over a decade ago, LLPAs were designed to protect the government-sponsored enterprises (GSEs) from borrower default risk.

But in May 2023, the FHFA implemented a revamped pricing matrix that sparked swift political and industry criticism. Critics argued that the updated structure penalized borrowers with high credit scores by reducing the price gap between them and borrowers with weaker profiles.

The move quickly became a flashpoint in housing policy. Headlines across the country accused the FHFA of flipping the script on creditworthiness. While that interpretation was an oversimplification, the perception stuck—and backlash followed.

Clarifying the 2023 LLPA Changes

The FHFA has maintained that the 2023 LLPA updates did not penalize borrowers with strong credit scores. Instead, the goal was to adjust the pricing framework to address long-standing disparities and make mortgage financing more accessible to historically underserved groups. Borrowers with higher credit still received better pricing overall, but the spread between top-tier and mid-tier credit profiles was narrowed—not reversed.

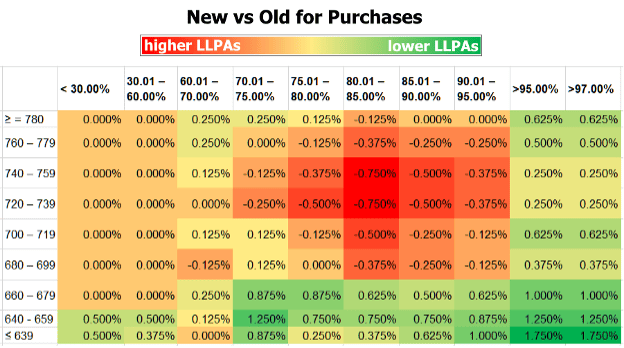

That said, many borrowers—particularly those with credit scores in the 680–740 range and down payments below 20%—did see increased fees. These mid-tier profiles often include first-time homebuyers and working families who might not benefit from subsidies but also don’t qualify for premium pricing. The visual breakdown of LLPA fees helped fuel public confusion and controversy, especially as media outlets began suggesting that strong-credit borrowers were being “penalized” under the new structure.

A Shift in Direction Under New Leadership

Fast forward to 2024, and the policy winds are shifting. New FHFA Director Bill Pulte—a Trump appointee—has made clear that he views the 2023 LLPA framework as flawed and politically motivated. His office recently released a statement indicating that a rollback of LLPA changes is under review, with public input actively being solicited.

In a move drawing support from lawmakers on the right, Pulte is framing the reversal as a return to fairness and financial accountability.

“We’re working to ensure that responsible borrowers—those who have done everything right—are not subsidizing risk they didn’t create,” said one senior FHFA official.

The Mortgage Bankers Association and other industry groups have voiced tentative support for the rollback, citing renewed affordability challenges in 2024. With mortgage rates still elevated and housing supply constrained, any reduction in upfront fees could be meaningful for today’s buyers.

What Would a Rollback Actually Save Borrowers?

While no formal LLPA rollback matrix has been published, housing analysts estimate that LLPA fees currently range from 0.25% to over 2% of the total loan amount, depending on credit score and down payment.

For a borrower taking out a $350,000 mortgage, that could mean savings of up to $3,500 or more upfront if certain fees are eliminated.

“This isn’t just about politics—it’s about affordability,” noted one policy analyst. “Reducing these fees could be the difference between qualifying and not for thousands of middle-income buyers.”

LLPA Changes 2024: Timeline and What’s Next

| Year | LLPA Milestone |

|---|---|

| 2020–2022 | Targeted LLPAs introduced on second homes and investment properties |

| May 2023 | New pricing framework implemented; criticism emerges |

| Early 2024 | Bill Pulte confirmed as FHFA Director |

| April 2024 | Public comment period opens to review potential rollback |

| Mid-2024 (est.) | FHFA expected to release updated pricing guidelines |

The FHFA is currently accepting public feedback through its website. A formal update to the LLPA matrix is expected later this year, depending on the volume and sentiment of responses.

Public Sentiment: Split But Vocal

Not everyone is on board. Housing advocacy groups have warned that undoing the 2023 changes could disproportionately impact borrowers of color and first-time homebuyers. The National Housing Conference has urged the FHFA to maintain the core structure of the revised pricing system, citing long-standing equity gaps in mortgage lending.

Meanwhile, borrowers with mid-to-high credit scores are voicing support for the rollback, especially those who saw fee increases despite qualifying for conventional financing.

“I’ve worked hard to maintain an 800+ score, only to be told it barely helps me anymore,” wrote one commenter on the FHFA’s portal.

Recap: What’s at Stake

- LLPAs are upfront fees based on borrower risk, applied by Fannie Mae and Freddie Mac.

- In 2023, FHFA revised its pricing to reduce disparities, but critics said it penalized qualified borrowers.

- New FHFA leadership in 2024 is reviewing a possible rollback.

- A rollback could save borrowers thousands in upfront fees.

- Public input is currently being accepted and may influence future LLPA policy.