History of Mortgages: How Home Loans Have Evolved

The history of mortgages is more than just a financial tale — it’s a window into the evolution of homeownership, economic policy, and societal priorities. From ancient roots to the digital lending era, mortgage systems have shifted dramatically to reflect how we value property, risk, and opportunity.

Ancient and European Origins of Mortgages

The term “mortgage” comes from the Old French words mort (dead) and gage (pledge), meaning a “dead pledge.” This early form of secured loan first appeared in ancient Rome, where people used land as collateral. Later, in medieval England, mortgages became legal agreements that transferred land ownership until debts were fully repaid.

Although these systems were very different from today’s loans, they laid the foundation for modern mortgage structures.

Mortgages in 19th and Early 20th Century America

In the United States, home loans remained informal for much of the 1800s. At the time, local banks and private lenders often issued land contracts with short repayment terms and large balloon payments at the end.

This approach functioned during periods of growth. However, when the Great Depression hit, defaults and foreclosures increased rapidly. The flaws in the system became impossible to ignore.

The New Deal and the Birth of Modern Mortgages

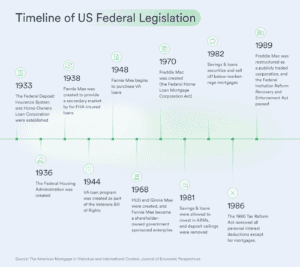

In response to the mortgage crisis, the U.S. government introduced a series of reforms in the 1930s. The creation of the Federal Housing Administration (FHA) in 1934 played a crucial role in stabilizing the market. The FHA made loans more accessible by promoting longer terms, lower down payments, and standardized repayment structures.

Further review: HUD’s history of the FHA

At the same time, the government established the Federal National Mortgage Association (Fannie Mae) to inject liquidity into the system. With more capital available, banks could offer more affordable home loans.

The Post-War Boom and Mortgage Standardization

Following World War II, the GI Bill provided returning veterans with access to affordable housing. Combined with the FHA and VA loan programs, this support helped create a massive surge in homeownership. As a result, the 30-year fixed-rate mortgage became the most common loan type.

This post-war boom transformed the idea of homeownership into a core part of the “American Dream.”

The Subprime Crisis and Housing Collapse

By the early 2000s, the mortgage market had changed dramatically. Lenders increasingly approved subprime mortgages for borrowers with low credit scores. In many cases, they didn’t require income verification.

These risky loans included adjustable-rate mortgages (ARMs) and were bundled into mortgage-backed securities. Eventually, the system collapsed. The 2008 housing crash caused millions to lose their homes and triggered a global financial crisis.

Recovery and the Rise of Consumer Protections

In the aftermath, lawmakers passed new regulations. The Dodd-Frank Act and the creation of the Consumer Financial Protection Bureau (CFPB) brought major changes. Lenders now had to confirm a borrower’s ability to repay, and transparency became a legal requirement.

During this time, Private Mortgage Insurance (PMI) also became more common for borrowers with lower down payments.

(Anchor text: private mortgage insurance (PMI) → internal article on PMI)

Modern Mortgages: Tech, Transparency, and Customization

Today, mortgage lending blends tradition with digital tools. Borrowers can compare rates online, use calculators, and apply in minutes.

Further review: Homebuying process in modern America

Technology has made it easier to understand complex details, including interest rates and amortization schedules.

In contrast to the past, the modern mortgage process now emphasizes education, personalization, and speed.

Looking Ahead: The Future of Mortgages

As technology advances, mortgage lending will continue to evolve. We may see the rise of AI-driven underwriting, blockchain for title verification, and new lending products focused on affordability.

Still, challenges remain. Housing access, sustainable lending, and financial literacy will remain central issues in the years ahead.

Final Thoughts

Understanding the history of mortgages helps consumers appreciate how far the industry has come. From ancient “dead pledges” to app-based loans, the mortgage has undergone major transformation. Learning about its evolution can empower today’s borrowers to make smarter, more informed decisions.