Mortgage lending has shaped the American dream for generations — but it wasn’t always the standardized, accessible system we know today. From early land contracts to the rise of federal housing programs and the 2008 financial crisis, the history of mortgage lending in the U.S. is a story of evolution, regulation, and resilience.

This article walks through the key milestones that redefined how Americans finance homeownership — and what they mean for borrowers today.

Early 1800s–1900: The Foundations of Private Lending

In the 19th century, mortgage lending was informal and unregulated. Wealthy individuals or local banks would issue short-term, interest-only loans — usually requiring 50% down or more.

Key characteristics:

-

Terms typically lasted 3–5 years

-

Balloon payments were common

-

Mortgages were not easily accessible to the working class

Foreclosure was common during economic downturns, and loans lacked federal oversight.

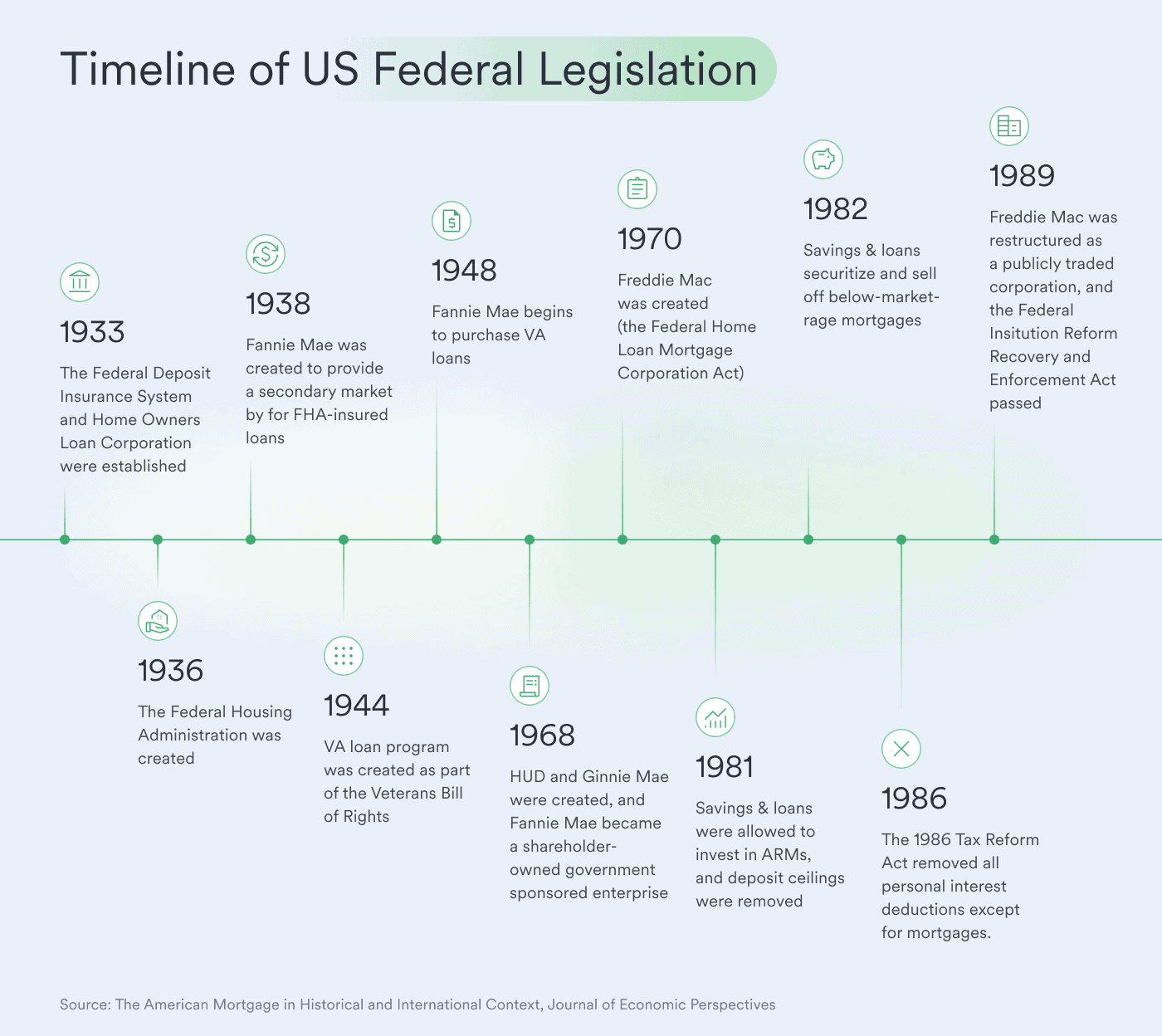

1920s–1930s: Collapse and Reform During the Great Depression

By the 1920s, mortgages became slightly more accessible, but the system was still unstable. When the Great Depression hit, millions of borrowers defaulted.

In response, the U.S. government launched sweeping reforms that would shape modern mortgage lending.

Key developments:

-

1934: Federal Housing Administration (FHA) established

-

Standardized mortgage lending

-

Introduced long-term, fixed-rate loans

-

Made low down payments possible

-

-

1938: Fannie Mae created to buy FHA loans and create liquidity for lenders

These programs made homeownership accessible to millions of working Americans for the first time.

1940s–1960s: Postwar Boom and Government-Backed Lending

The end of WWII triggered a massive housing boom — and new federal programs made lending even easier.

Key events:

-

1944: GI Bill / VA Loan Program offered 0% down loans to returning veterans

-

30-year fixed-rate mortgages became the norm

-

Suburban development exploded, especially among white Americans (redlining and racial disparities in lending persisted)

By 1960, over 60% of Americans owned homes — up from 40% in the 1930s.

1970s–1980s: Inflation, Securitization, and the S&L Crisis

Rising inflation and interest rates in the 1970s disrupted traditional mortgage lending. In response, new systems were created to encourage liquidity and investor confidence.

What changed:

-

1970: Freddie Mac was created to support a secondary mortgage market

-

1981–1982: Mortgage rates peaked at over 18%

-

Adjustable-rate mortgages (ARMs) entered the market

Meanwhile, deregulation of the Savings & Loan (S&L) industry led to risky behavior — resulting in over 1,000 S&L institutions failing by the end of the 1980s.

1990s–2000s: Growth, Deregulation, and the Subprime Boom

The 1990s ushered in technological innovation and rapid growth. Lending guidelines loosened, and securitization made it easier to approve non-traditional borrowers.

Red flags:

-

Subprime lending surged

-

Low-doc and no-doc loans became common

-

Housing demand outpaced supply, fueling a bubble

By 2006, homeownership hit an all-time high — but cracks in the system were already forming.

2008–2010: The Mortgage Crisis and Financial Collapse

The 2008 financial crisis was largely triggered by risky mortgage lending practices. When housing prices collapsed, millions of Americans faced foreclosure.

Fallout:

-

Lehman Brothers collapsed

-

Major banks required federal bailouts

-

Home values dropped by 30%+ in some markets

Congress passed the Dodd-Frank Act to regulate the lending and banking industries more tightly. The Consumer Financial Protection Bureau (CFPB) was created in 2011.

2010s–Today: Regulation, Technology, and Homeownership Gaps

Modern mortgage lending has become safer and more standardized — but challenges remain.

Key trends:

-

Stricter underwriting rules post-crisis

-

Mortgage tech (e-signatures, online preapprovals) streamlined the process

-

Racial and socioeconomic homeownership gaps persist

-

Affordability challenges have returned in many markets due to low inventory and rising rates

Today, the mortgage system is safer, but also more complex than ever.

FAQ: History of Mortgage Lending

When did mortgage lending become common in the U.S.?

The modern mortgage system began to take shape in the 1930s with the creation of the FHA and Fannie Mae.

What caused the 2008 mortgage crisis?

The crisis was triggered by a rise in risky subprime loans, inflated home values, and investor demand for mortgage-backed securities.

How did the government fix mortgage lending after the crash?

Regulatory reforms like Dodd-Frank and the creation of the CFPB increased transparency, lender accountability, and borrower protections.

Who created the 30-year fixed mortgage?

The FHA introduced the 30-year fixed mortgage in the 1930s to make homeownership more affordable and predictable.

Is mortgage lending safer today than in the past?

Yes — post-2008 regulations have tightened lending practices, although new risks (like affordability) have emerged in recent years.

Final Thoughts

The history of mortgage lending in the U.S. reflects broader economic cycles, government intervention, and changing consumer needs. What started as a private, informal arrangement has evolved into a highly regulated system — one that balances accessibility with risk management.

Whether you’re applying for an FHA, VA, or conventional loan, understanding this history helps you see why today’s lending rules exist — and where the future may lead.

Related Posts

What Affects Mortgage Rates? Key Factors That Influence What You Pay

When you’re planning to buy a home or refinance, one of the most important questions is: What affects mortgage rates? While the number

What Credit Score Do You Need to Buy a House?

When you’re preparing to buy a home, one of the first questions to ask is: what credit score do you need to buy

History of the Mortgage

History of Mortgages: How Home Loans Have Evolved The history of mortgages is more than just a financial tale — it’s a window