FICO, long dominant in the mortgage credit scoring industry, is now at the center of an intensifying controversy. On May 20, 2025, FHFA Director Bill Pulte publicly criticized Fair Isaac Corporation — the creators of FICO scores — for “jacking up” credit score costs. His remarks triggered a sharp selloff in FICO stock, which dropped over 20% in two days, marking its steepest decline since March 2020.

This latest blow has sparked broader debate around credit report pricing, FICO’s near-monopoly in tri-merge reporting, and the growing call for alternatives like VantageScore 4.0.

FICO Stock Reacts to Public Criticism

Following Pulte’s remarks on X (formerly Twitter), FICO’s stock tumbled:

- -8.1% on May 20

- -14% on May 21

View full data →

This reflected market concerns not only about public perception but also about upcoming changes to credit scoring policy driven by the Federal Housing Finance Agency (FHFA). Investors and analysts are now reevaluating the long-term profitability of FICO’s credit report royalties and its entrenched position in mortgage underwriting.

A Longstanding Monopoly in Transition

FICO’s credit scoring model has underpinned nearly every mortgage decision for decades. Through the “tri-merge” process — combining reports from Equifax, Experian, and TransUnion — lenders rely on FICO to evaluate borrower creditworthiness. Despite the existence of models like VantageScore, FICO’s stronghold has limited meaningful competition.

However, change is coming.

FHFA and VantageScore 4.0: A Push for Reform

In late 2022, the FHFA approved both a bi-merge credit report system and the adoption of VantageScore 4.0 for loans purchased by Fannie Mae and Freddie Mac. These changes are set to take effect in late 2025 and are designed to:

- Encourage competition in the credit scoring space

- Improve consumer inclusivity and fairness

- Reduce overall costs for lenders

A recent release of historical VantageScore data by the GSEs has further legitimized the model. VantageScore 4.0 incorporates more modern credit behaviors, considers rental payments, and uses machine learning to reduce bias. This has made it especially appealing to underserved borrowers often penalized by legacy models.

More on this → FHFA Policy on Credit Scores

Mortgage Lenders Face Rising Credit Report Costs

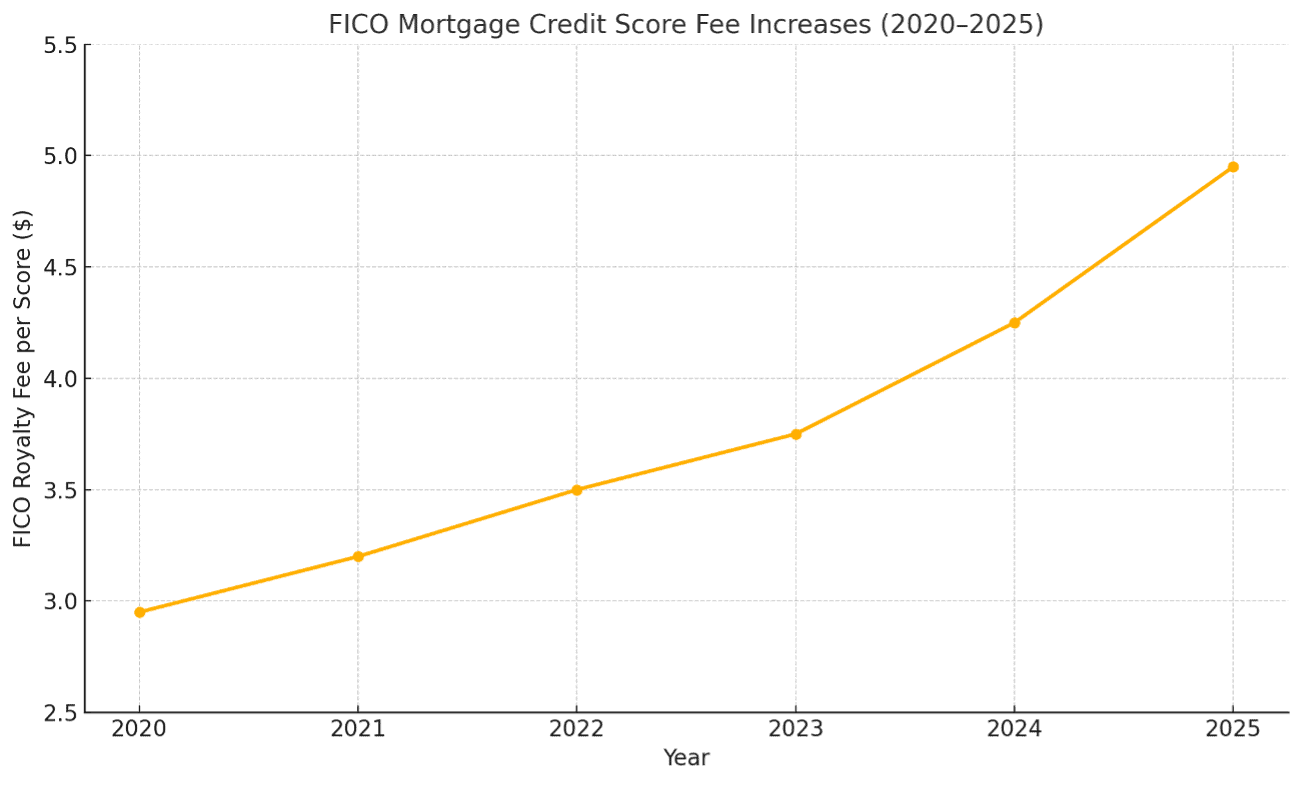

At the heart of the controversy is FICO’s pricing model. The wholesale royalty fee charged by FICO has risen from $3.50 to $4.95 per score — a 41% increase. For a tri-merge credit report, this translates to nearly $9 more per borrower on joint applications.

Lenders have reported cost increases across both hard pulls (formal loan applications) and soft pulls (pre-qualifications). In some cases, soft pull reports now cost up to $30, with no longer any discounting from credit bureaus.

Smaller lenders, which typically eat this cost upfront, are shifting the burden to consumers, charging $50–$100 per report just to apply. For homebuyers already struggling with affordability, this adds another barrier to entry.

The Trigger Lead Problem

Meanwhile, FICO’s pricing is just one of many grievances. Another hot-button issue is trigger leads — a practice in which credit bureaus sell borrower data to other lenders after a credit report is pulled. This leads to:

- Unwanted solicitations

- Privacy concerns

- Confusion among consumers mid-mortgage process

In response, over 125 mortgage professionals gathered in Washington, D.C., this April to advocate for the Homebuyers Privacy Protection Act (H.R. 2808). The bill seeks to restrict trigger lead use and protect borrower information during mortgage applications.

Where’s FICO in All This?

As of this writing, FICO has not issued a public response to the FHFA Director’s statements. In prior years, the company has defended its royalty pricing model, saying it reflects the value provided to lenders and that its scoring system supports a strong, fair mortgage market.

But with rising regulatory scrutiny, a push for competitive models, and a vocal FHFA leadership, FICO’s position in the mortgage ecosystem may face fundamental change.

What This Means for Borrowers and the Industry

Consumers should expect:

- Possible relief on credit report fees by late 2025

- Greater transparency and fewer marketing solicitations (if trigger lead reforms pass)

- New scoring models that better reflect modern borrowing behavior

Lenders will need to adjust to:

- A dual scoring system transition`

- Pricing pressure from borrowers unwilling to pay upfront for reports

- The operational shift from tri-merge to bi-merge standards

One thing is clear: The era of unquestioned dominance by FICO in mortgage underwriting is ending. And the FHFA, under Pulte’s leadership, seems determined to make that transition happen sooner than later.